IN THIS ARTICLE

Community Banks Are Disappearing. Here's What Actually Leaves When They Go.

Springfield’s diner on Main Street needed a $150K construction draw from their line of credit to get a new kitchen. The owner had banked at the same institution for 20 years. The local bank’s lender had known him since middle school. He understood what that diner meant to the town, and a draw got approved by Friday.

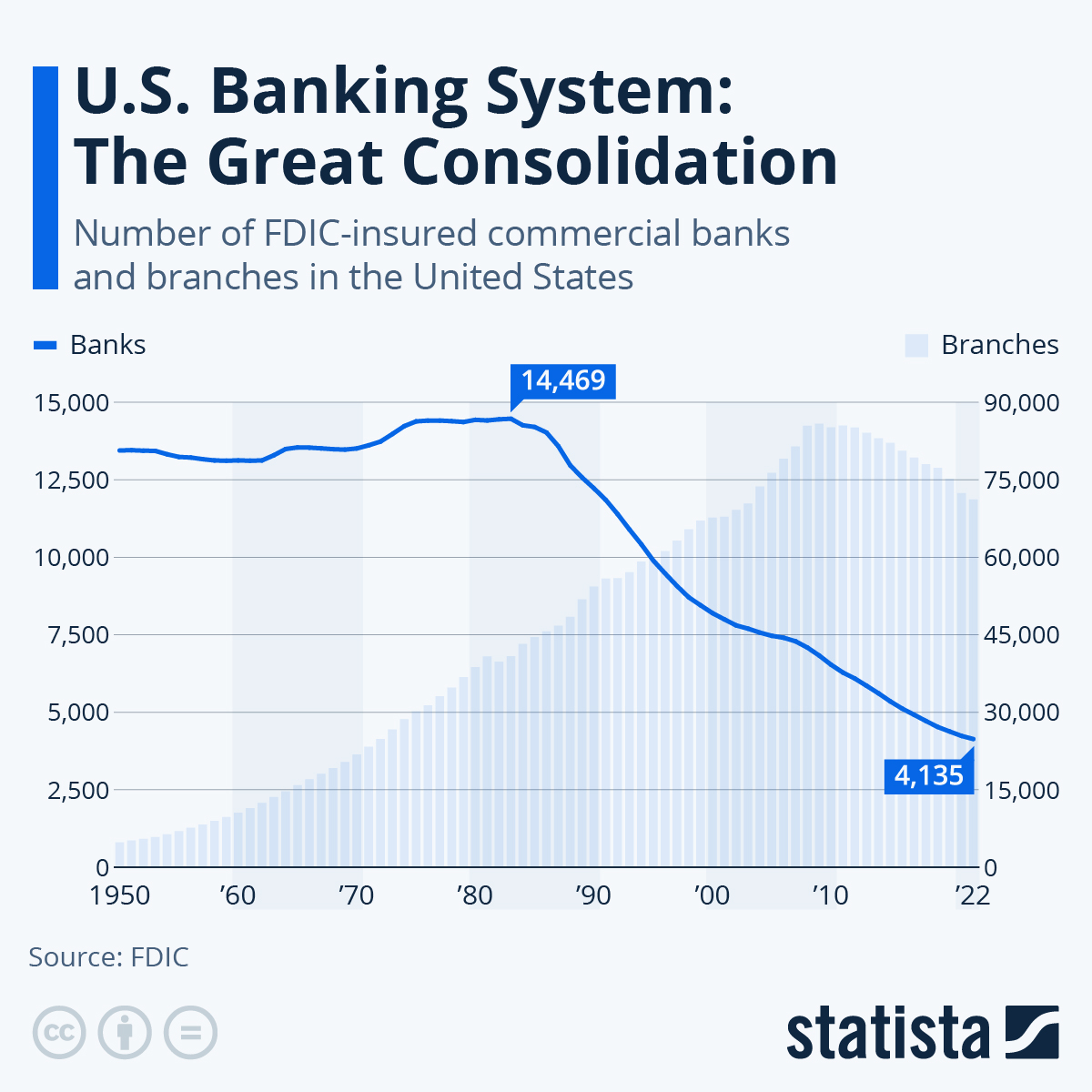

Now, in the last 25 years, the number of FDIC-insured commercial banks in the U.S. has fallen by 53%. The press releases call it consolidation. What they don't mention is that the next time that diner needs a draw, it's going through a centralized underwriting team three states away that has never met the owner.

What Gets Lost That Nobody Counts

When a community bank gets acquired, the location often remains.

What actually walks out the door: the president, the CFO, the operations leaders. These are the kind of anchor roles that keep professional talent rooted in a community rather than relocating to a metro — important local decision-making authority.

Then go the mid-level positions: the loan officers, the branch managers, the credit analysts who grew up down the road and chose to stay. Then the teller jobs, the administrative staff, the back-office roles that a local family counted on.

Beyond the jobs, the capital changes behavior. Deposits that once circulated locally — funding the hardware store's line of credit, the contractor's equipment loan, the dentist's office expansion — now flow into a regional institution with different priorities and a different geographic footprint.

A banker I spoke with who has worked across both large and community institutions put it plainly: "I have yet to be involved with a large bank institution that made the lending process quick, smooth, and painless." It's not that bigger banks lack the appetite. It's that their back-office can't support the speed. Draw requests, percent-complete calculations, multi-party approvals — the work that community lenders handle by feel gets buried in a system designed for scale, not judgment.

The relationship disappears because the human capital that makes it possible usually doesn’t stay.

The Succession Problem Nobody's Solving

Most consolidation gets framed as a competitive story. Big banks win on scale, technology, and distribution.

That framing misses the quieter reason a lot of these institutions are gone.

They didn't fail. They ran out of people willing to run them.

The pattern repeated throughout the early 2000s and accelerated after the financial crisis: a founder passes away. The family looks at what they've inherited — examination cycles, capital requirements, BSA compliance, fair lending reviews — and makes a rational calculation. Sell. Not because the bank wasn't profitable. Because the operational burden had never been made manageable enough to hand off.

A former FDIC examiner who watched this play out firsthand described it plainly: "The family doesn't want to deal with it, the Board doesn't want the regulatory burden. Best bet, sell it off."

That's not a story about a bank that failed its community. It's a story about an institution that never unlocked the operational infrastructure that would have made succession possible. The deposits were there. The relationships were there. The processes to sustain them beyond a couple generations — that's what hadn't been built yet.

The Regulatory Cost Is Real. It's Also Not the Whole Story.

The compliance cost argument deserves to be taken seriously. Community banks pay federal income taxes and carry full regulatory overhead while competing against credit unions operating without the same tax burden — and credit unions have quietly expanded their product offerings and membership eligibility to the point where the structural difference is harder to defend than it used to be.

On pure cost economics, that's a real disadvantage. It's not an invented grievance.

But it also can't explain everything, because community banks operating under the same regulatory environment are also consolidating. The ones that are winning haven't found a workaround for compliance costs. They've found a different way to compete.

What Some Bankers Are Betting On

When we talk to bankers about differentiation, the conversation used to land on vague territory — "relationships," "local knowledge," "white-glove service." Lately, it's getting more specific.

A former Chief Lending Officer we spoke with framed it this way: the banks that win won't be targeting the general public. They'll be targeting a distinct niche, understanding that niche's needs better than anyone, and building products specifically designed around it.

His examples were more specific than you'd expect. Direct-pay dentists. Blended families navigating complex financial situations. Gig workers. The further down the stack, the better — because the more specific the niche, the harder it is for a bank with 400 branches to replicate.

We're not saying this is the only path. But it's an option worth taking seriously, especially for institutions trying to figure out where to compete rather than trying to compete everywhere at once.

The Tech Question Worth Asking

The conversation about community bank technology usually collapses into two bad extremes: either you need to match big-bank infrastructure to survive, or technology is a threat to the human element that makes you valuable.

The more productive question is simpler: what are your best bankers spending time on that they shouldn't have to?

Here's the line that seems to matter. On one side: the basics — mobile access, online banking, the digital product set clients now expect as a baseline. Community banks that haven't matched big banks here are losing customers before a relationship even starts. That's table stakes, not differentiation.

On the other side: the judgment. The credit decision that requires knowing the borrower's history. The draw approval that requires understanding the project. The loan structure that requires context a system can't have.

The bet some community bankers are making is moving toward automating that second category — using AI-driven pre-approval processes that remove human back-office work from decisions that used to require it.

The goal isn't automation for its own sake. It's freeing up the bankers you already have — the ones with the judgment — to spend their time on the work only they can do.

What the Banks That Survive Are Doing Differently

Construction lending. Agricultural credit. Treasury management for a specific industry. A niche defined tight enough that it becomes a genuine competitive advantage — not a positioning statement.

One banker put it simply: "You have to have bankers who care about the success of a local business — not just the stock price of the company they work for."

The deposits that should stay in your institution are already in your market. The relationships are already there. The question is whether your back-office can support the bankers who know how to keep them.